The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

Right now, all eyes are on the Fed. Most economists expect they'll cut the Federal Funds Rate at their mid-September meeting to try to head off a potential recession.

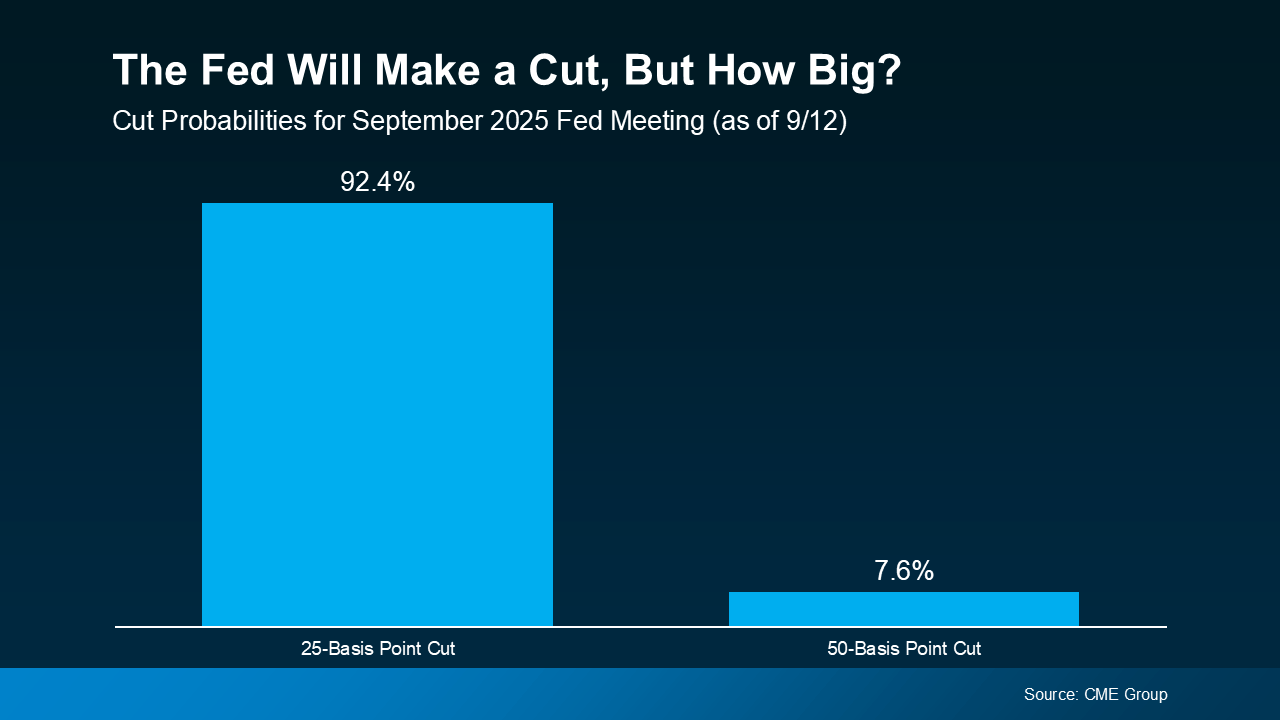

According to the CME FedWatch Tool, markets are already betting on it. There’s virtually a 100% chance of a September cut. And based on what we know now, there’s about a 92% chance it’ll be a small cut (25 basis points) and an 8% chance it will be a bigger cut (50 basis points):

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

Here’s the part that may surprise you. Mortgage rates tend to respond to what the financial markets think the Fed will do, before the Fed officially acts. Basically, when markets anticipate a Fed cut, that outlook gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Each time, mortgage rates ticked down as financial markets grew more confident a cut was coming soon. And even though inflation rose slightly in the latest CPI report, the Fed is still expected to make a cut.

So, if the Fed goes with a 25-basis point cut, as expected, that’s likely already baked in to current mortgage rates, and we may not see a dramatic drop.

But if they go bigger and drop their Federal Funds Rate by 50 basis points instead, mortgage rates could come down more than they already have.

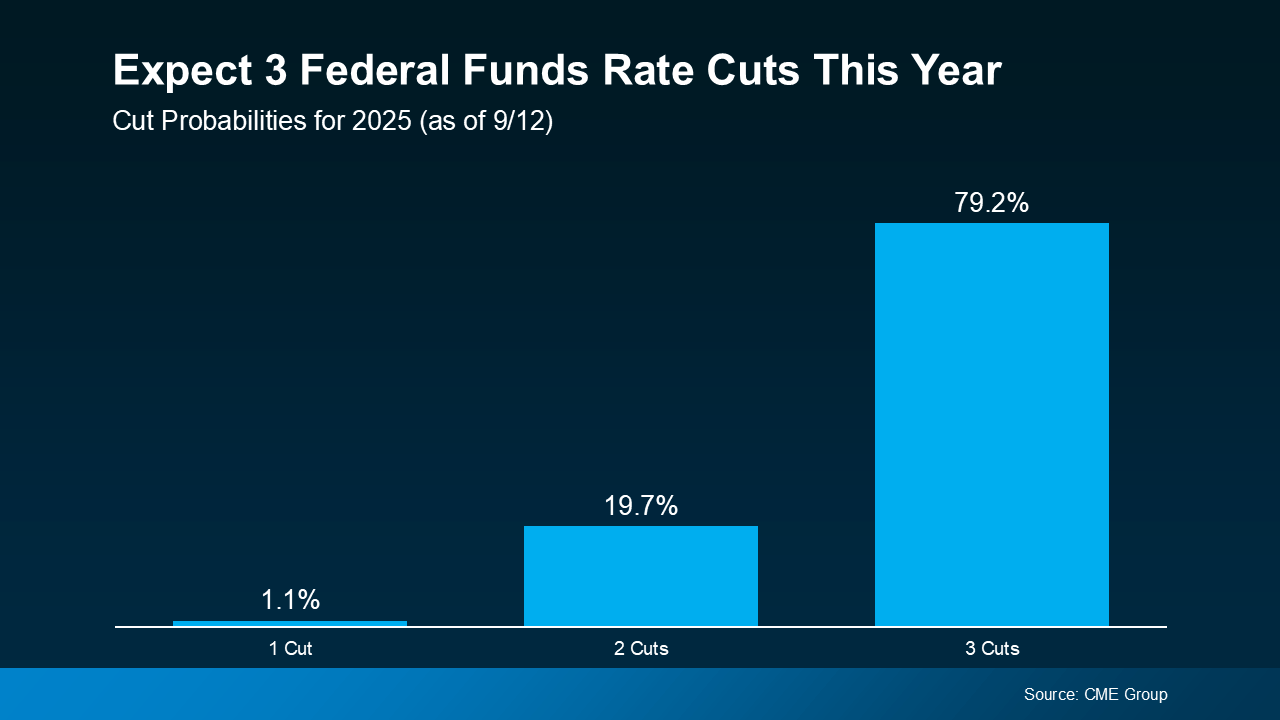

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that’s if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple rate cuts happen, or even if markets just believe they will, mortgage rates could ease further in the months ahead. But here’s the catch – all of this depends on how the economy evolves. Surprise inflation data or unexpected shifts could quickly change the outlook.

Mortgage rates likely won’t drop sharply overnight, and they won’t mirror the Fed’s moves one-for-one. But if the Fed begins a rate-cutting cycle, and markets continue to expect it, mortgage rates could trend lower later this year and into 2026.

If you’ve been waiting and watching the housing market, now’s the time to talk strategy. Even small changes in rates can make a meaningful difference in affordability, and understanding what’s ahead helps you make the best decision for your situation.

I’m Nadine Lutz, one of Atlanta's top Realtors and a trusted Atlanta, Georgia Real Estate Agent with Compass Buckhead, and Atlanta has been home to my family since 2003. Over the years, I’ve been blessed to help so many neighbors achieve their real estate goals, and I’m honored to be recognized with the Phoenix Award and as a Multi-Million Dollar Club Life Member with the Atlanta Realtors Association.

Awards aside, what matters most to me is guiding people through one of the biggest decisions of their lives with honesty, care, and local expertise. If you’re ready to explore Atlanta homes for sale or make your next move, I’d be grateful for the chance to help.

Q: Does a Fed rate cut mean my mortgage rate automatically drops?

No. Mortgage rates don’t move in lockstep with the Fed. They respond to investor expectations and broader economic data.

Q: When could we see meaningful changes in mortgage rates?

If the Fed signals multiple cuts ahead, or if markets believe they’ll follow through, mortgage rates could gradually trend lower into 2026.

Q: Should I wait to buy a home until rates drop?

Waiting is a gamble. Rates may trend lower, but housing demand and prices could shift too. Talking to a trusted advisor can help weigh your options.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Check out the latest articles on real estate trends.

Lifestyle

Fast, loud, and nothing like traditional tennis, INTENNSE is bringing a high-energy sports entertainment experience to Assembly Atlanta with nonstop action, timed matches, music, and electric crowd energy.

Lifestyle

A massive indoor mega slide, towering drop ride, jungle gym, and carnival-style thrills are officially coming to Atlanta, and adrenaline seekers are already obsessed.

Lifestyle

Atlanta’s beloved Lantern Parade is making its long-awaited comeback in Fall 2026 after weather forced the event’s cancellation in 2025.

Lifestyle

A new fan-driven study from Men in Blazers highlights the best places to eat, drink, and explore in Atlanta during the FIFA World Cup, and the city is proving why it’s one of America’s top soccer destinations.

Lifestyle

Atlanta foodies and culture lovers can experience Asian street food, live entertainment, local vendors, and immersive community vibes at this free one-night-only AAPI Night Market event.

Lifestyle

Just 90 minutes from ATL, Lake Lanier combines sandy beaches, floating obstacle courses, and summer lake vibes into one unforgettable holiday weekend getaway.

Lifestyle

Atlanta’s newest hidden rooftop experience combines luxury dining, skyline views, craft cocktails, and upscale nightlife into one unforgettable evening.

Address

3107 Peachtree Rd NE A-1

Atlanta GA 30305